Before you can determine the date at which you can securely retire, you need to create your own personal balance sheet. Here’s how.

Creating a personal balance sheet does not require an MBA. All it takes is a little organization, finding the time, and some arithmetic.

The first step is establishing your net worth. Your net worth is simply the difference between what you own and what you owe. This is what I call your personal balance sheet.

In accounting, everything that you own is known as your assets. And what you owe others is collectively known as your liabilities. The difference is your net worth, and you will rely on this number throughout your retirement years.

Once you begin keeping your personal balance sheet up to date on a regular basis (I recommend once a year), you will be able to see trends that you hadn’t noticed before while making sure that you are on the right track toward meeting the retirement goal you set for yourself.

First, let’s get acquainted with different types of assets.

Asset Categories

-

Current Assets

Investments

Retirement Accounts

Real Estate

Business

Current Assets

Current assets are the assets that you can quickly convert into cash (liquidate) if necessary. You should be able to liquidate these assets in about one year or less.

Current assets include:

Savings accounts

Checking accounts

Certificates of deposit (CDs)

Investments

Investments are assets that you purchase with the expectation that they will generate income in the future and/or be sold at a higher price than they were purchased for. Do not include investments within your individual retirement account (IRA) in this category.

Investments include:

Stocks

Bonds

Mutual Funds

Retirement Accounts

Retirement accounts come in many shapes and sizes, and they are each beholden to their own regulations. They all are designed to provide sources of income after retirement, and they each have unique tax rules and exemptions.

Retirement accounts include:

401k

IRA

Roth IRA

Pension Plans

Employee Stock Ownership Plans (ESOPs)

Real Estate

As for your real estate, that is becoming easier to value using Zillow.com. Zillow may not accurately get your home value correct. The more unique or out of the way your home is the more likely Zillow will value your home incorrectly.

Business

If you own real estate or own your own business, you will have to do some of your own work. Best to speak to your accountant or seek outside advice on how you should value your business.

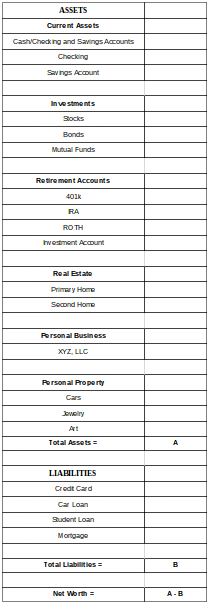

Here’s an example of a simple spreadsheet you can create to calculate your own net worth (click to enlarge):

Personally, I update the balance sheet annually at the end of each year. The personal balance sheet is a great way to understand your financial position in concrete terms. Simply taking this fiscal snapshot regularly over time allows you to see trends and plan for the future. Next week, I’ll discuss how to forecast what you’ll need for retirement using your personal balance sheet.

James Cornehlsen, CFA, is a Portfolio Manager at Capstone Investment Financial Group.